What To Do To Get Monetarily Audio Home Mortgages

Content written by-Drachmann GottliebBefore getting a mortgage, you must first take many steps. Before anything else, learn all that you can about the process of securing a loan. That starts with the following paragraphs and the useful knowledge within them.

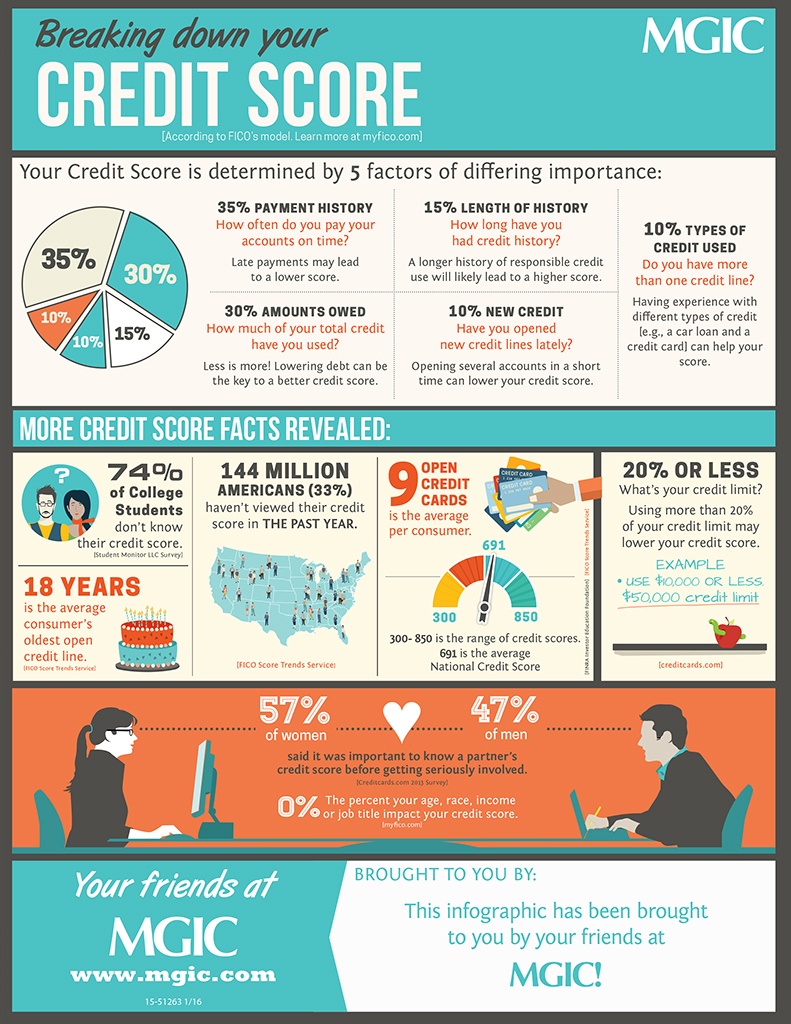

Before getting a mortgage, study your credit history. Good credit is what can help you get a mortgage. Obtain copies of your credit history and scores from the three major credit-reporting bureaus. Study your reports carefully to ensure that no issues or errors must be resolved before you apply. Many lenders need a minimum score of 680, which complies with Freddie Mac and Fannie Mae's guidelines. Most lenders want to avoid scores that are lower than 620.

Understand your credit score and how that affects your chances for a mortgage loan. Most lenders require a certain credit level, and if you fall below, you are going to have a tougher time getting a mortgage loan with reasonable rates. A good idea is for you to try to improve your credit before you apply for mortgage loan.

Try to have a down payment of at least 20 percent of the sales price. In addition to lowering your interest rate, you will also avoid pmi or private mortgage insurance premiums. This insurance protects the lender should you default on the loan. Premiums are added to your monthly payment.

If your mortgage has been approved, avoid any moves that may change your credit rating. Your lender may run a second credit check before the closing and any suspicious activity may affect your interest rate. Don't close credit card accounts or take out any additional loans. Pay every bill on time.

Find out how much your mortgage broker will be making off of the transaction. Many times mortgage broker commissions are negotiable just like real estate agent commissions are negotiable. Get this information and writing and take the time to look over the fee schedule to ensure the items listed are correct.

When you decide to apply for a mortgage, make sure you shop around. Before deciding on the best option for you, get estimates from three different mortgage brokers and banks. Although, interest rates are important, there are other things you should consider also such as closing costs, points and types of loans.

Keep your job. Lenders look into many aspects of your financial situation and one very important aspect is your employment income. Stability is very important to lenders. Avoid moving jobs or relocating for as long as possible before you apply for a home mortgage. This will show them that you are stable.

If your mortgage is for thirty years, making additional payments can help you pay it off more quickly. This will pay off your principal. If you pay more regularly, you are going to cut down the interest you need to pay, and you'll be able to be done with your loan that much faster.

Do not accept an interest rate that is variable. The interest on these loans can vary greatly depending on the economic climate. This may mean that you can no longer afford your house, which is what you don't want to happen.

If you are a retired person in the process of getting a mortgage, get a 30 year fixed loan if possible. Even though your home may never be paid off in your lifetime, your payments will be lower. Since you will be living on a fixed income, it is important that your payments stay as low as possible and do not change.

If you have a little bit more money to put down on a home, consider getting a conventional mortgage as opposed to an FHA mortgage. FHA mortgages have lower down payments, but excessive fees that are added to the cost of the mortgage. Save up at least 5 percent in order to be eligible for an FHA loan.

Go online and use a mortgage calculator to find out how much of a loan you can afford. There are https://www.globenewswire.com/news-release/2021/11/18/2336969/0/en/ABN-AMRO-intends-to-appoint-Annerie-Vreugdenhil-as-CCO-Personal-Business-Banking-and-member-of-the-Executive-Board.html that offer these free calculators. Additionally, there are calculators that will tell you the final price you will be paying at the end of the loan and others that show how much you can save by paying extra toward the principal.

Be realistic when choosing a home. Just because your lender pre-approves you for a certain amount doesn't mean that's the amount you can afford. Look at https://news.bloomberglaw.com/business-and-practice/deutsche-banks-ex-americas-legal-chief-leaving-top-trust-role and your budget realistically and choose a home with payments that are within your means. This will save you a lifetime of stress in the long run.

If your mortgage is up for renewal, you should consider other lenders. As long as your mortgage isn't renewed, you won't face any penalties for switching to another company, unless there is a fee for paying off the mortgage in full. Thankfully, most lenders will cover that cost just for moving to them.

If you are able to personally afford a little bit higher monthly payment towards your mortgage, then a 15-year loan might not be a bad option. These short-term loans have lower interest rates and monthly payments that are slightly higher in exchange for the shorter loan period. You might be able to save thousands of dollars by choosing this option.

Pay your mortgage down faster to free up money for the future. Pay a little extra each month when you have some extra savings. When you pay the extra each month, make sure to let the bank know the over-payment is for the principal. You do not want them to put it towards the interest.

If you need to make repairs to your home you may want to consider a second home mortgage. As long as you have a good history of paying on time you should be able to get a great rate, and by improving your home you are increasing its value. Just be sure that you will be able to make the payments.

Never choose a home mortgage from a company that asks you to do unscrupulous things. If a rep is asking you to claim more than you make to secure the mortgage, it's not a good sign that your mortgage is in good hands. Walk away from these deals as quickly as you can.

It is critical that you have an understanding of home mortgages when purchasing your first home. Comprehending all details helps ensure you get a good deal. Make sure you focus on the details, using these tips to ensure maximum results from your loan.